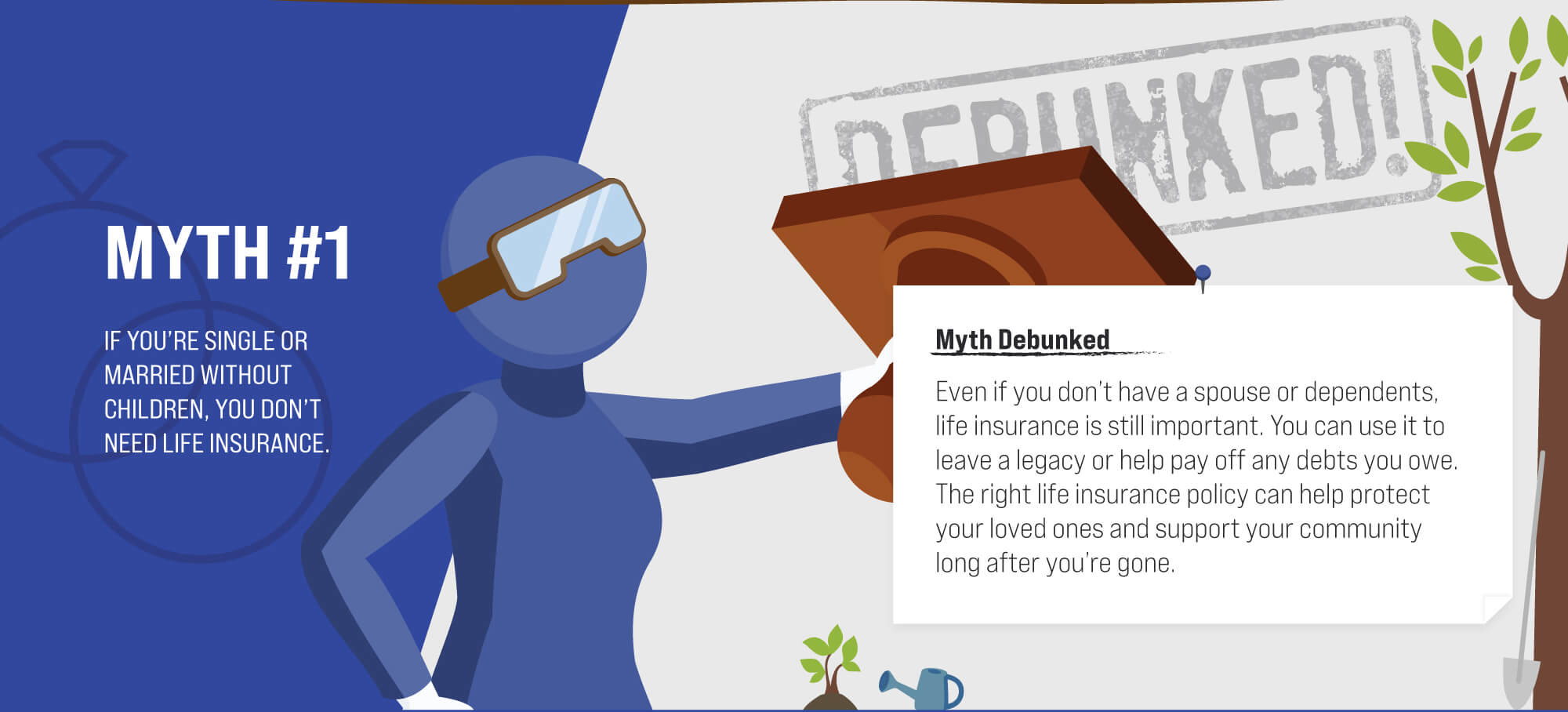

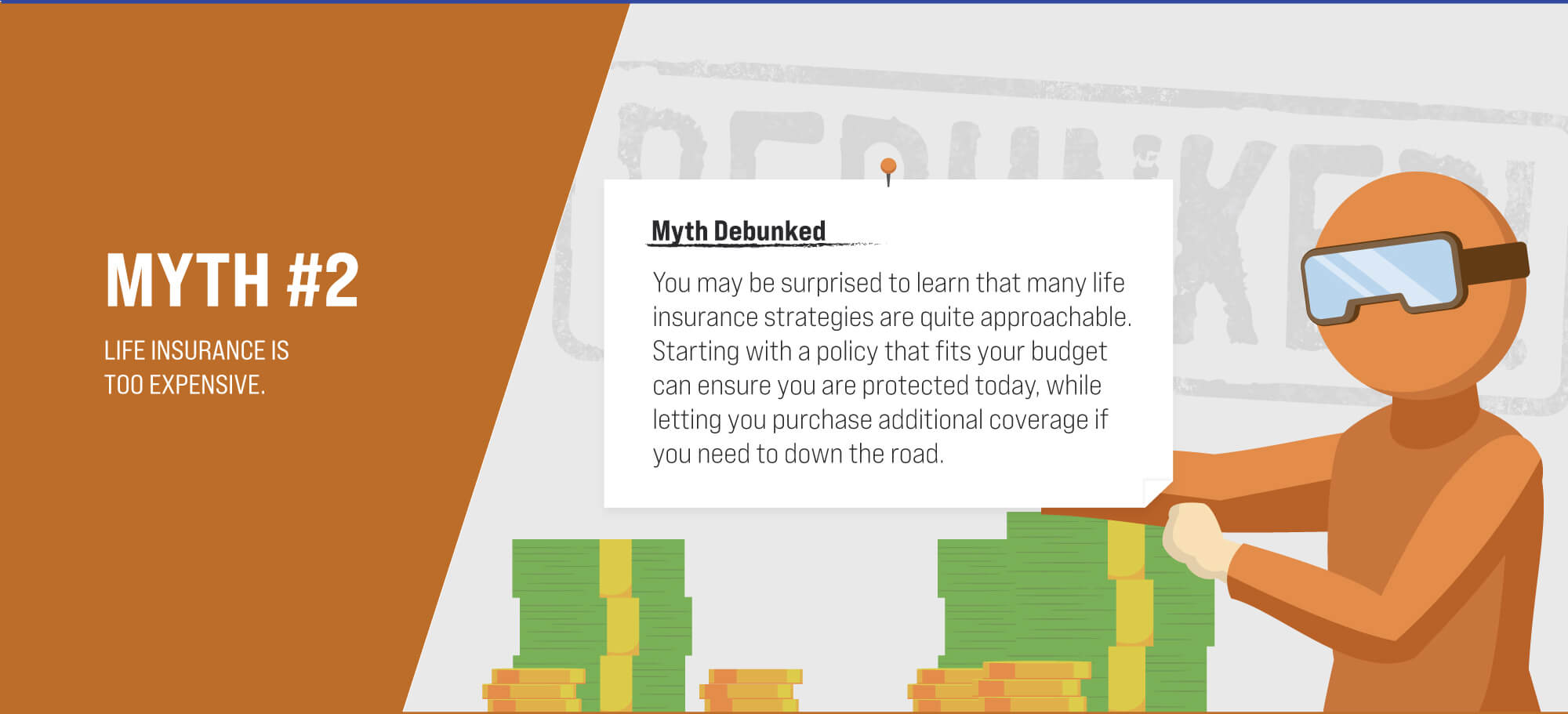

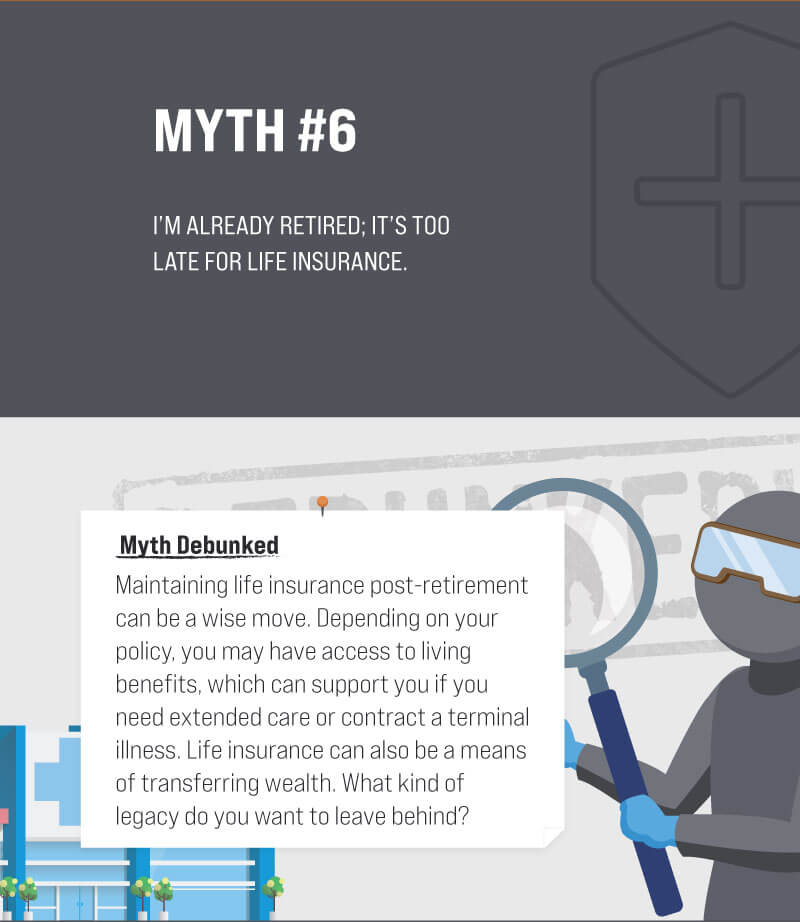

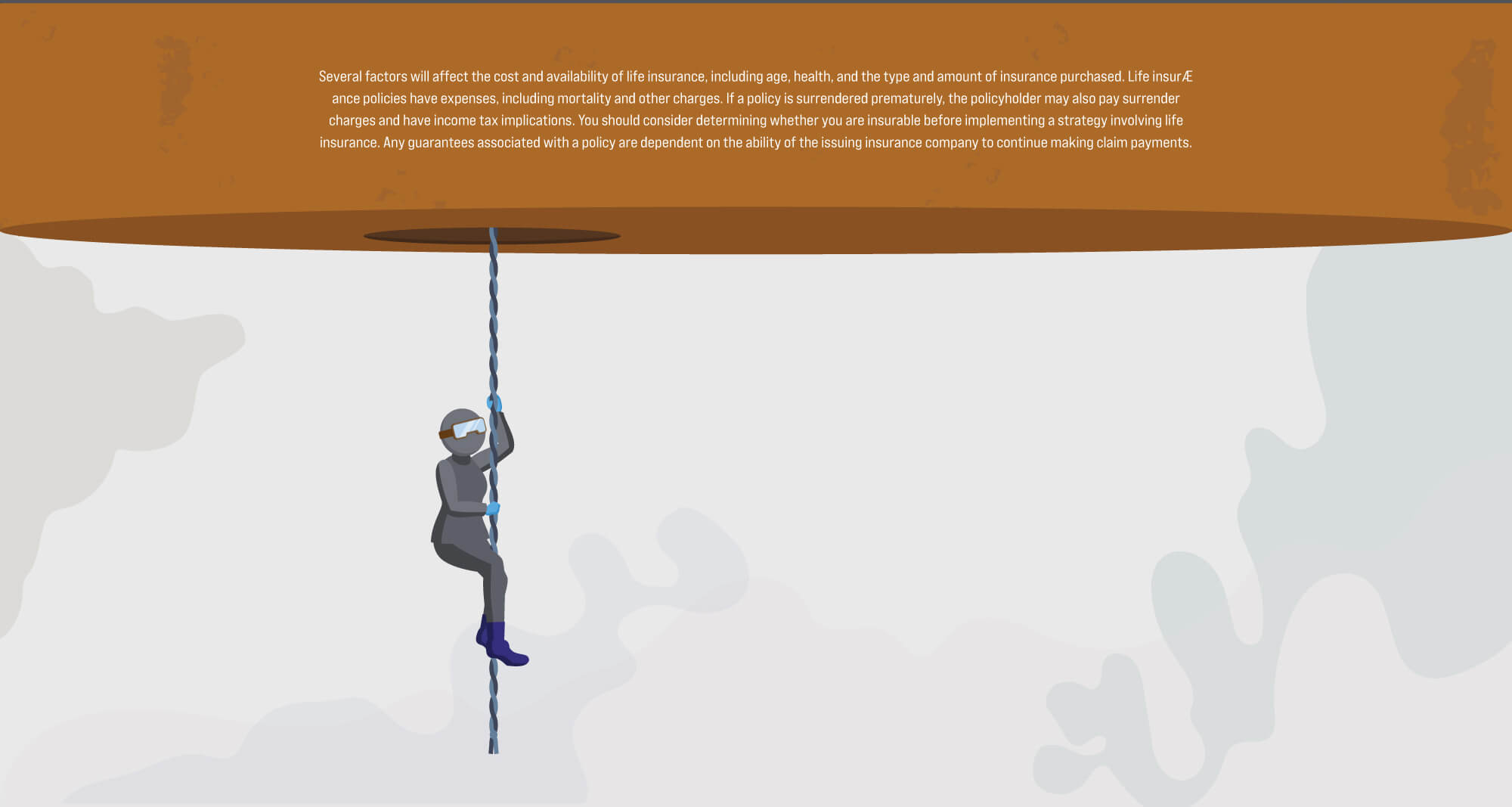

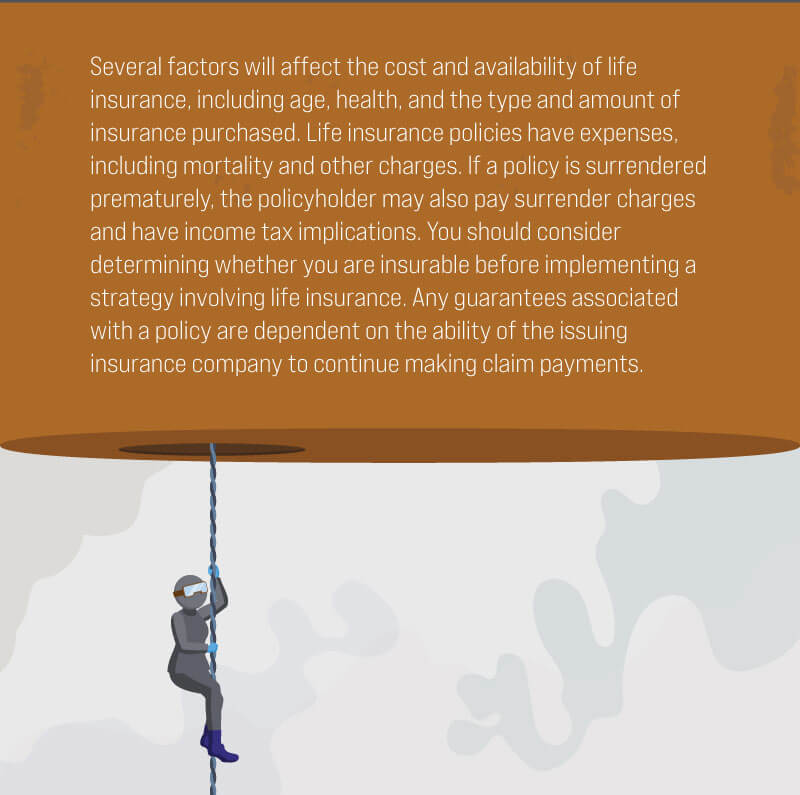

Insurance Life Insurance Myths: Debunked Have A Question About This Topic? Name Email Address Question Thank you! Oops!